글로벌 대표적인 소비재 기업입니다.

시가총액은 약 278조 원입니다.

2021년 기준으로 신발 매출이 63%, 의류 매출이 약 29%입니다.

지역별 매출은 미국이 가장 높은 약 39%, EMEA(Europe, Middle East and Africa)는 약 26%입니다.

매출은 16% 성장했으나 기대(컨센서스) 대비 아쉽게 발표되어 6%이상의 급락이 있었습니다.

주당순이익 EPS는 기대(컨센서스)대비 잘 나왔습니다.

실적

EPS (주당순이익)은 기대보다 0.04달러 높은 1.16달러로 발표되었습니다.

Revenue (매출)은 기대보다 225.13M 달러 낮은 12.25B달러가 발표되었습니다.

지난 분기에는 EPS가 컨센서스 대비 매우 높은 실적이 발표되어 실적 발표 후, 약 15.5% 상승이 있었습니다. (21.6.25)

이슈

EPS가 양호한데 매출 이슈로 인해 급락이 있었습니다.

베트남에서 코로나로 인해 신발 생산을 6월 이후 10주째 못 하고 있습니다.

10월부터 재생산 예정입니다.

악재입니다.

향후 실적에도 영향을 줄 수 있습니다. 그러나 해결될 것입니다.

Matthew Friend — Executive Vice President and Chief Financial Officer

Consumer demand for NIKE remains at an all time high and we are confident that our deep consumer connections and brand momentum will continue. However, we are not immune to the global supply chain headwinds that are challenging the manufacturer and movement of product around the world. Previously, I had shared that we were planning for transit times to remain elevated for the balance of fiscal ’ 22. Unfortunately, the situation deteriorated even further in the first quarter with North America and EMEA seeing increases in transit times due primarily to port and rail congestion and labor shortages.

Additionally, several of our factory partners in Vietnam and Indonesia were required to abruptly cease operations in the first quarter. As of today, Indonesia is now fully operational, but in Vietnam nearly all footwear factories remain closed by government mandate. Our experience with COVID related factory closures suggests that reopening and ramping back to full production scale will take time. Therefore, we’re revising our short-term financial outlook to incorporate the following factors: 10 weeks of production already lost in Vietnam since mid July. Factory reopening to occur in phases beginning in October with a ramp to full production over several months and elevated transit times consistent with where we are now operating today.

We now expect fiscal ’22 revenue to grow mid single digits versus the prior year versus our prior guidance of low doubledigit growth due solely to the supply chain impacts that I just described. Specifically for Q2, we expect revenue growth to be flat to down low-single digits versus the prior year as factory closures have impacted production and delivery times for the holiday and spring seasons. Lost weeks of production combined with longer transit times will lead to short-term inventory shortages in the marketplace for the next few quarters.

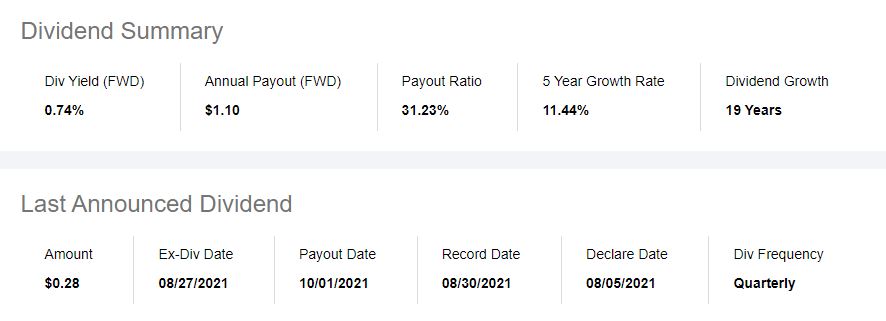

배당

연 배당률은 1% 미만으로 높은 건 아니지만 (0.7% 예상)

19년간 배당금을 증가시킨 배당성장주입니다.

분기배당입니다.

최근 분기 지급내역을 보면,

12월에 배당금이 증가되는 게 보입니다.

이번에도 공급 차질 이슈에도 불구하고 배당금을 증가시킬 수 있을까요?

0.22달러에서 0.245달러로 증가(11.4% 증가율)

0.245달러에서 0.275달러로 증가(12.2% 증가율)

약 11% 증가율을 적용하면, 약 0.305달러를 예상할 수 있습니다.

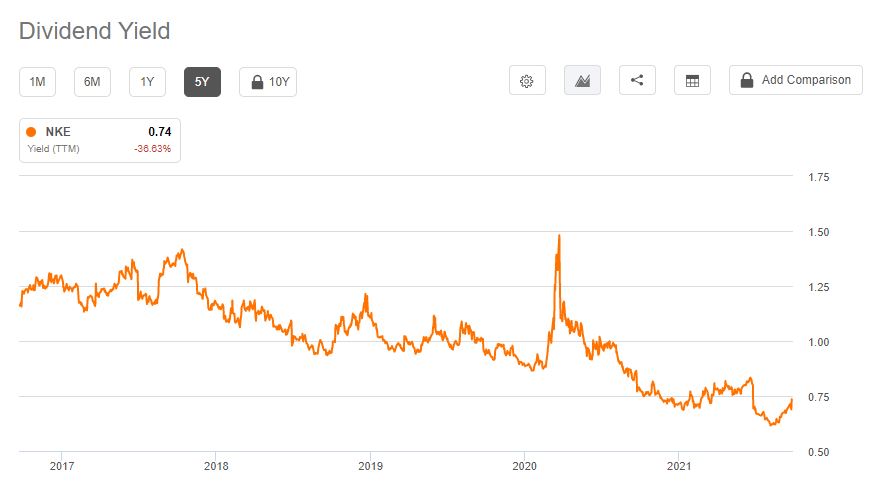

최근 5년 배당률을 보면,

배당금이 증가했는데도 불구하고 주가 상승이 더 커서 배당률이 낮습니다.

주가 흐름

올해 주가 흐름입니다.

지난 6월 말 호실적으로 주가가 급등하고 약 175달러까지 올라갔다가 조정받은 모습입니다.

S&P500지수를 추종하는 ETF인 SPY(검은색)과 비교해보았습니다.

8월부터 조정으로 인해 상대적으로 아쉬운 모습입니다.

그런데 2년의 흐름으로 확장해보니

지수 대비 좋습니다. 다만 중간중간 인고의 시간이 필요했습니다.

향후 전망

브랜드 가치에 손상은 없습니다.

공급 차질 이슈도 결국은 해결될 것입니다.

단, 악재이며 예상보다 늦게 해결될 수도 있습니다.

긴 호흡으로 조금씩 모아가기에는 괜찮아 보입니다.

감사합니다.

*투자에 참고하시되, 매매에 대한 판단은 스스로 하시길 바랍니다.

'주식' 카테고리의 다른 글

| 구글 ETF : 주식분할로 관심이 높아진 구글 (0) | 2022.07.19 |

|---|---|

| ETF 세금 : 미국 상장 ETF, 한국 상장 ETF (0) | 2022.01.08 |

| 테슬라 ETF : 테슬라를 가장 많이 보유한 ETF는? (1) | 2022.01.06 |

댓글